What happens if you measure hedge fund returns properly?

Issue 1 · The Model Is Not the Market — Gate 1: do the numbers mean anything?

Every strategy conversation opens the same way: someone shows you a number. A curve, a Sharpe, a monthly table. The instinct is to interrogate the strategy behind it. The first gate is duller than that — interrogate the number itself.

This exploration has a dual purpose — to make you doubt yourself from the outset, but to also understand you are in good company. The industry that has thrown billions of dollars and many thousands of PhDs at this problem is struggling to clear this gate, too.

by Joachim Klement originally published at

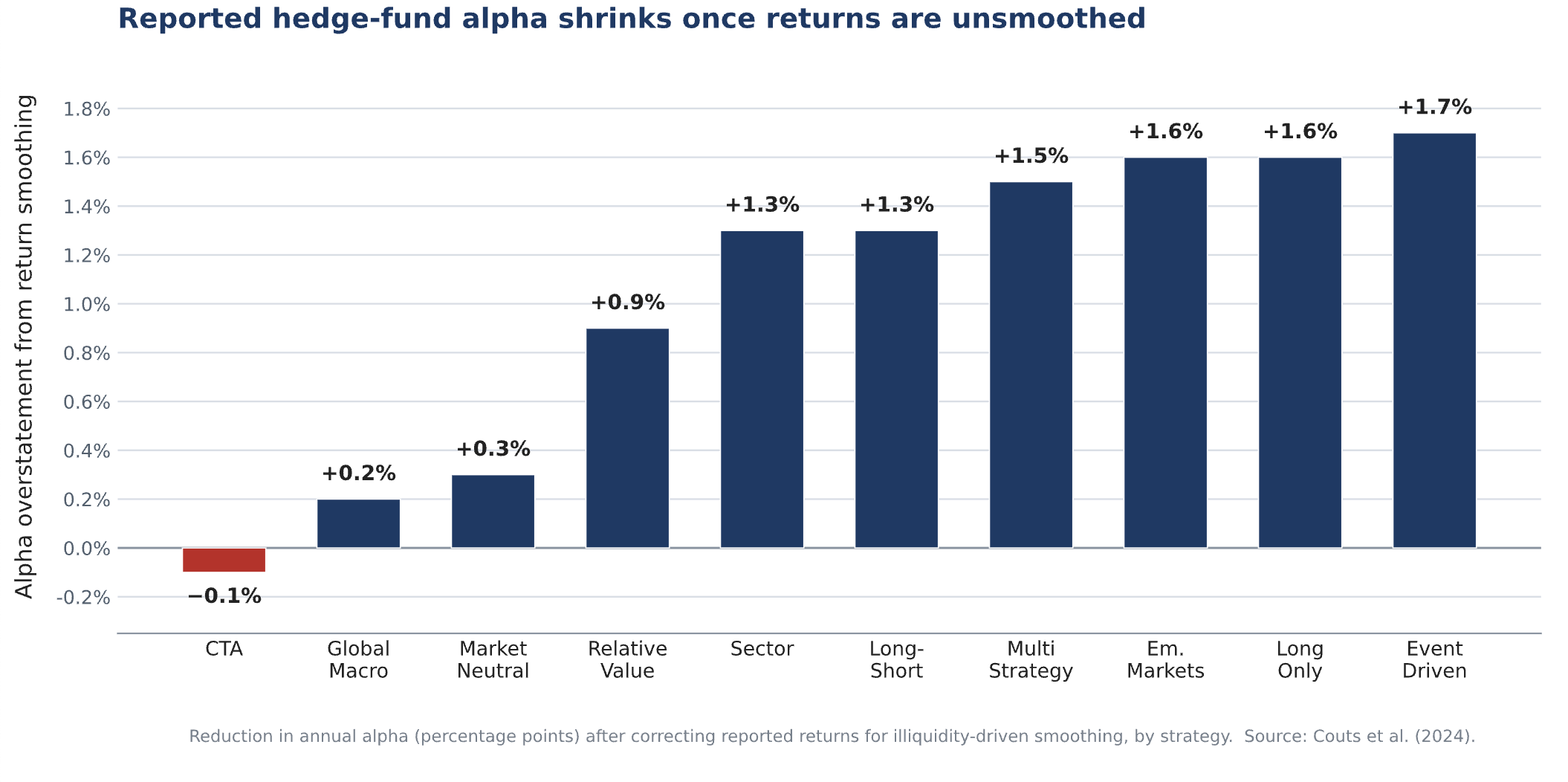

One of the eternal problems with measuring the return and risk of private investments is that the lack of liquidity artificially smooths return over time. This in turn creates the impression of a very good risk-return trade-off. But not only that. If one compares these smoothed returns to the return of listed investments like stocks and bonds, it appears as if hedge funds have skill (i.e. alpha) where there is none. It’s like the old illusion that many private investors suffer from where they believe that investing in real estate is very lucrative and has few risks compared to stock markets. Their views would likely change if their properties were valued and reported on TV daily.

Spencer Couts and his colleagues have gone through an elaborate exercise to unsmooth the returns of hedge funds and check what that implies for the alpha these hedge funds achieve vs. listed stocks and bonds. The chart below shows the reduction in hedge fund alpha by strategy from the raw alpha reported by hedge funds, collected in databases, and reported in the news to the true alpha they have achieved.

Alpha bias in different hedge fund strategies.

Source: Couts et al. (2024)

Note that most hedge fund strategies overreport their alphas by about 1.5% per year. Only the most liquid strategies like macro hedge funds, CTA, and equity market neutral show little to no bias.

If we correct hedge fund returns from this bias, then it changes which hedge fund strategies have true alpha and which ones don’t. Long-short hedge funds, for example, on average report an annual alpha of 1.5%, but that disappears completely when the true volatility of the underlying investment portfolio is taken into account. Long only, emerging market, and sector specialist hedge funds even end up with negative alpha on average, meaning on average it’s better to just go with an index fund than these vehicles. And that is before costs!

Meanwhile, the three hedge fund strategies with the highest positive alpha on average are relative value funds (though their alpha drops from about 3.3% p.a. to 2.5% p.a.) and macro and CTA hedge funds (both with an average alpha of about 2% p.a.). Event-driven and market-neutral funds have small positive alphas before fees, but the fees are much higher than these alphas, so investors end up with lower returns than simply going into a low-cost 60/40 stock/bond portfolio for example.

Joachim Klement writes every day. I highly recommend subscribing to him here:

And you can read the original piece here.